A single trunk can breach a roof, compromise structure, and turn a livable home — or a detached guest house — into a major rebuild decision overnight. On the North Shore and in Whistler, it happens more often than most homeowners expect.

Eurohouse Construction has responded to exactly this scenario in West Vancouver, including a project on Rosebery Avenue where a fallen tree caused sufficient structural impact that the right solution was to rebuild the guest house rather than patch a compromised shell. This article breaks down what typically happens, how insurance approaches it in British Columbia, and what homeowners can do to speed up recovery.

Why It's Common Here: North Shore & Sea-to-Sky Conditions

West Vancouver, North Vancouver, and Whistler share the same risk factors that make tree-on-structure incidents a recurring event rather than a freak occurrence.

- Tall, mature urban forest canopy — large conifers and deciduous trees throughout residential neighbourhoods

- Wind corridors during storm systems — the North Shore mountains funnel and accelerate winds

- Saturated soils after heavy rain — which reduces root stability, especially on slopes

- Steep lots and tight setbacks — where trees and buildings coexist in close proximity

Local wind events routinely bring down trees across the North Shore and Sea-to-Sky corridor. The frequency and cost of severe-weather insurance claims in Canada has risen sharply over the last decade — and this area is squarely in the zone.

The Real Damage Pattern When a Tree Hits a House

A "tree on roof" loss is rarely cosmetic. When a mature conifer or large limb hits a house, damage clusters into predictable categories.

1. Structural Breach and Water Intrusion

If the roof is opened — even by a few inches — rain follows immediately. Insurers commonly recognize wind-driven opening and the resulting water entry as part of the same loss scenario. Every hour of exposure compounds the damage.

2. Hidden Structural Compromise

Even when the exterior looks "repairable," tree impacts can twist ridge lines, crack truss plates, rack exterior walls, and overload beams and posts. This kind of damage isn't always visible without opening up the structure.

3. Secondary Damage and Escalation

Electrical mast damage, smashed glazing, flooded finishes, mold risk, and access constraints can push a "repair" into a "rebuild" business case quickly. The longer the structure sits exposed, the more the scope grows.

⚠ The First 48 Hours Matter

Treat the hours after a tree strike like a claim file is being built — because it is. Every photo, every tarp, every temporary protection measure becomes part of the record that determines your coverage outcome.

Repair vs. Rebuild: How the Decision Gets Made

Homeowners often ask: "Can we just fix the roof and move on?" Sometimes yes. But a full rebuild becomes the better option when:

- The structural system is compromised across multiple planes

- Moisture exposure is extensive and has reached framing, insulation, or finishes

- The building was older or non-compliant, and any significant repair triggers broader code upgrades

- The schedule risk of piecemeal restoration is higher than a clean replacement

That's exactly why some detached structures — like guest houses — end up being rebuilt. A purpose-designed replacement delivers faster certainty, cleaner compliance, and a result that performs long-term.

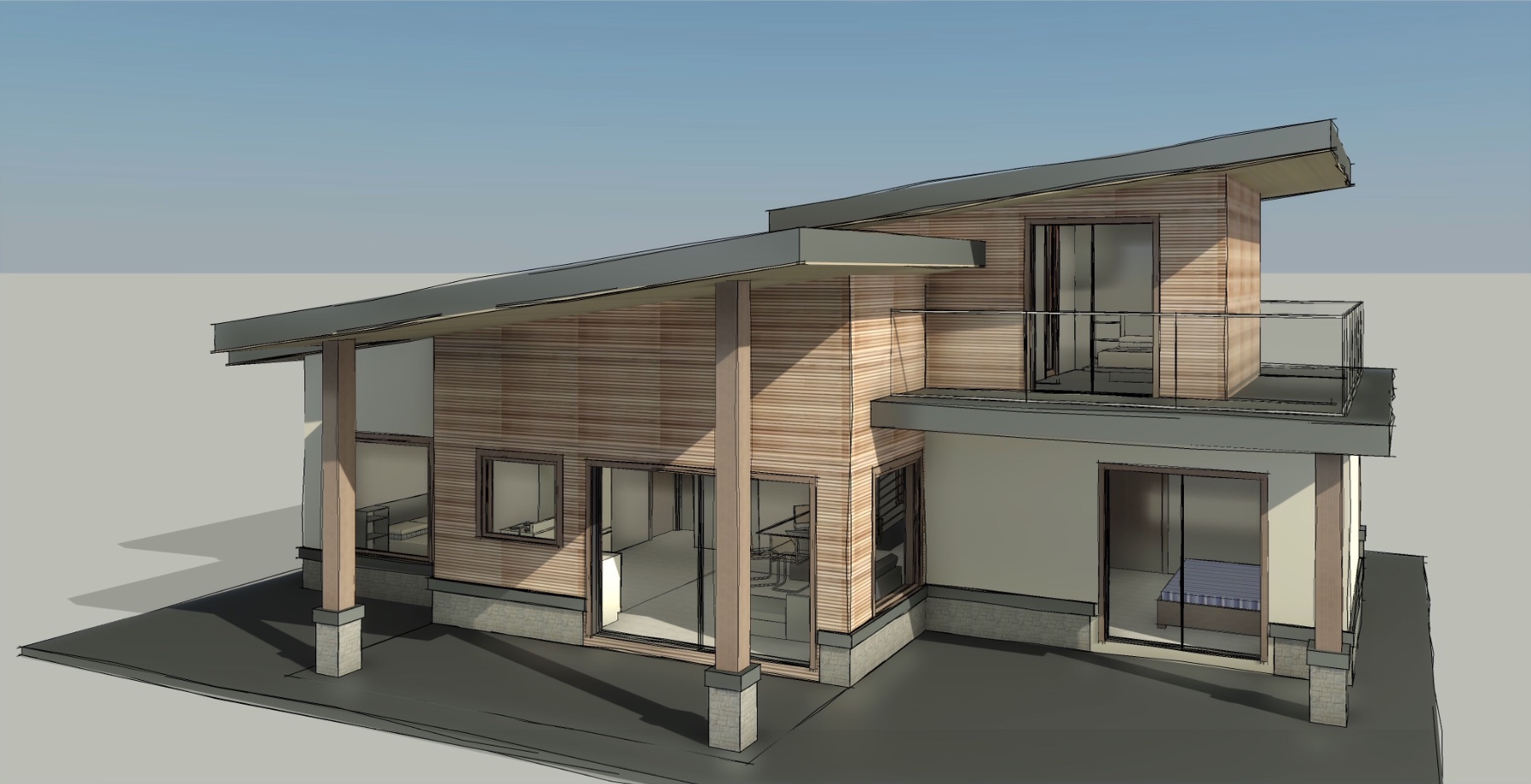

Case Snapshot: Rosebery Avenue Guest House Rebuild

- Cause: Mature tree fell during North Shore windstorm, striking detached guest house

- Damage: Roof structure breach, framing racked, rapid water intrusion

- Decision: Full rebuild — structural compromise too extensive for viable repair

- Process: Insurance coordination, architectural design, engineering, development permit, District design board review, neighbour consultation

- Result: Modern West Coast contemporary accessory dwelling — designed, permitted, and built by Eurohouse

Insurance in BC: What's Typically Covered

Most Canadian home insurance policies cover wind-related damage, including losses caused by falling branches or trees — subject to your deductible and policy limits. This generally applies whether the tree was on your property or a neighbour's.

What Can Complicate Coverage or Slow Approvals

- Neglect or known hazard: If the tree was clearly dead, rotting, or previously flagged and the owner failed to address it, insurers may challenge parts of the claim or raise liability questions

- Tree removal vs. building repair: Building repairs are usually straightforward under insurance. Tree removal and debris clearing can be capped or treated differently depending on your policy wording

- Scope uncertainty: Adjusters want a clear plan — temporary protection, safe demolition where required, and a defined rebuild or repair path. Vague or evolving scope slows everything down

You Can Choose Your Own Contractor

Even when your insurer is managing the claim, you have the right to bring in a qualified contractor of your choosing. Your policy covers the cost of restoration — it does not dictate who performs the work. A contractor experienced in insurance claims can manage documentation, scope approval, and adjuster communications on your behalf.

What to Do Immediately After a Tree Falls on Your Home

- Safety first. Assume live power, gas line risk, and unstable structure. Do not enter until it's been assessed.

- Stop further damage. Tarps, temporary shoring, weather protection — every hour of exposure adds to the scope.

- Document everything. Wide shots, close-ups, interior water paths, timestamps. Progressive photos over the first few days are especially valuable.

- Call your insurer early. Get a claim number and confirm emergency mitigation parameters before you spend money.

- Bring in the right contractor. You want a team that can manage structural assessment, restoration sequencing, permitting implications, and insurer communication — without drama.

How Eurohouse Approaches Tree-Impact Losses

When a tree hits a home in West Vancouver, North Vancouver, or Whistler, the goal is straightforward: stabilize fast, define scope accurately, and rebuild or restore to the level that was there — without shortcuts.

- Emergency stabilization and water control

- Structural review and transparent options (repair vs. rebuild)

- Tight estimating with supporting documentation for the insurer

- Design and permitting when rebuild is the right path — including District approvals, engineering, and neighbour consultation

- Construction execution with quality control on envelope, structure, and finishes

If your home includes higher-end assemblies — custom glazing, specialty cladding, European cabinetry — that's where contractor capability matters most. Replacement isn't "standard restoration." It requires sourcing knowledge, trade relationships, and craftsmanship that generic restoration crews don't typically bring.

Documentation Wins

Photos, temporary protection records, arborist notes if relevant, and a tight scope narrative. The quality of your initial documentation directly impacts how smoothly — and how fully — your claim gets resolved.